How Do Accidents Impact Car Insurance in Ontario?

If you’ve recently been involved in a motor vehicle accident, you’re likely wondering what will happen to your insurance premiums. In Ontario, a collision can raise your insurance costs at renewal (sometimes significantly) when you’re found to be at-fault for the accident.

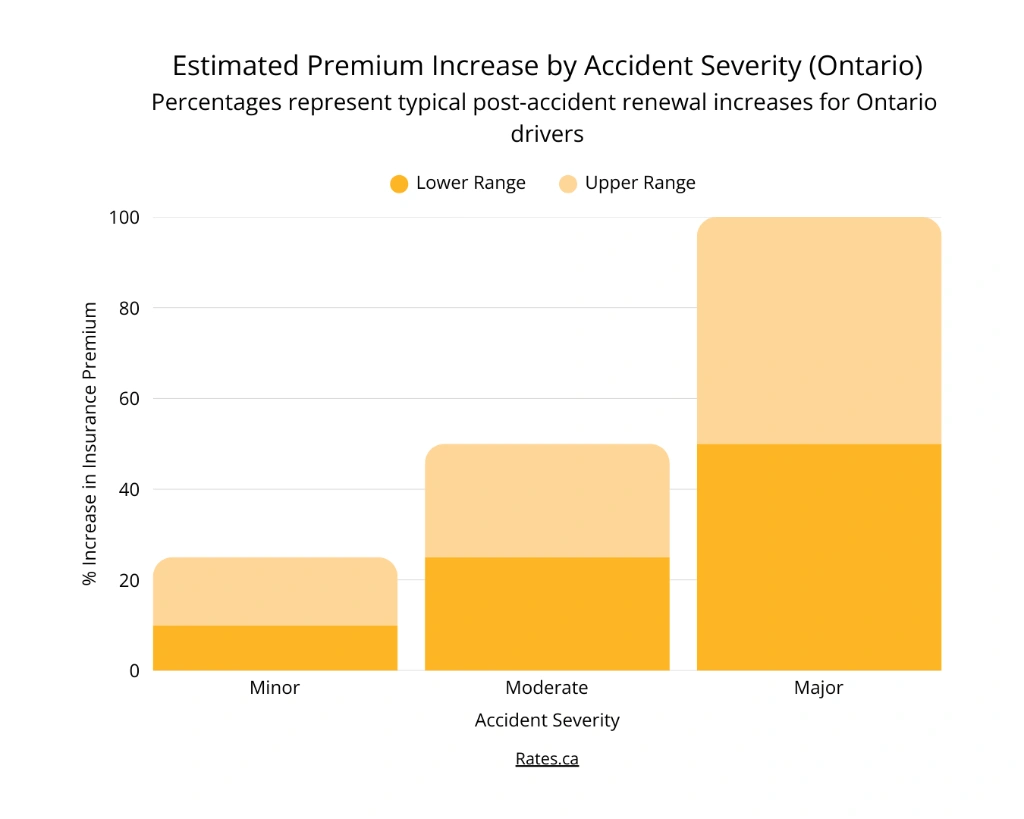

In 2025, an at-fault collision (50% or more fault) may increase premiums at renewal by 20%-50%, or sometimes more. For drivers already categorized as high-risk, surcharges can even reach 100% plus. These premium changes can remain on a driving and rating record for several years. By contrast, when a driver is 0% at fault for the accident, their premiums generally do not increase.

If you were injured in a collision in Ontario and have questions about fault, Statutory Accident Benefits, timelines, or next steps for pursuing compensation, contact our car accident lawyers for a free consultation. Our legal team can help you understand your rights and options in the event you’ve been injured in a motor vehicle accident.

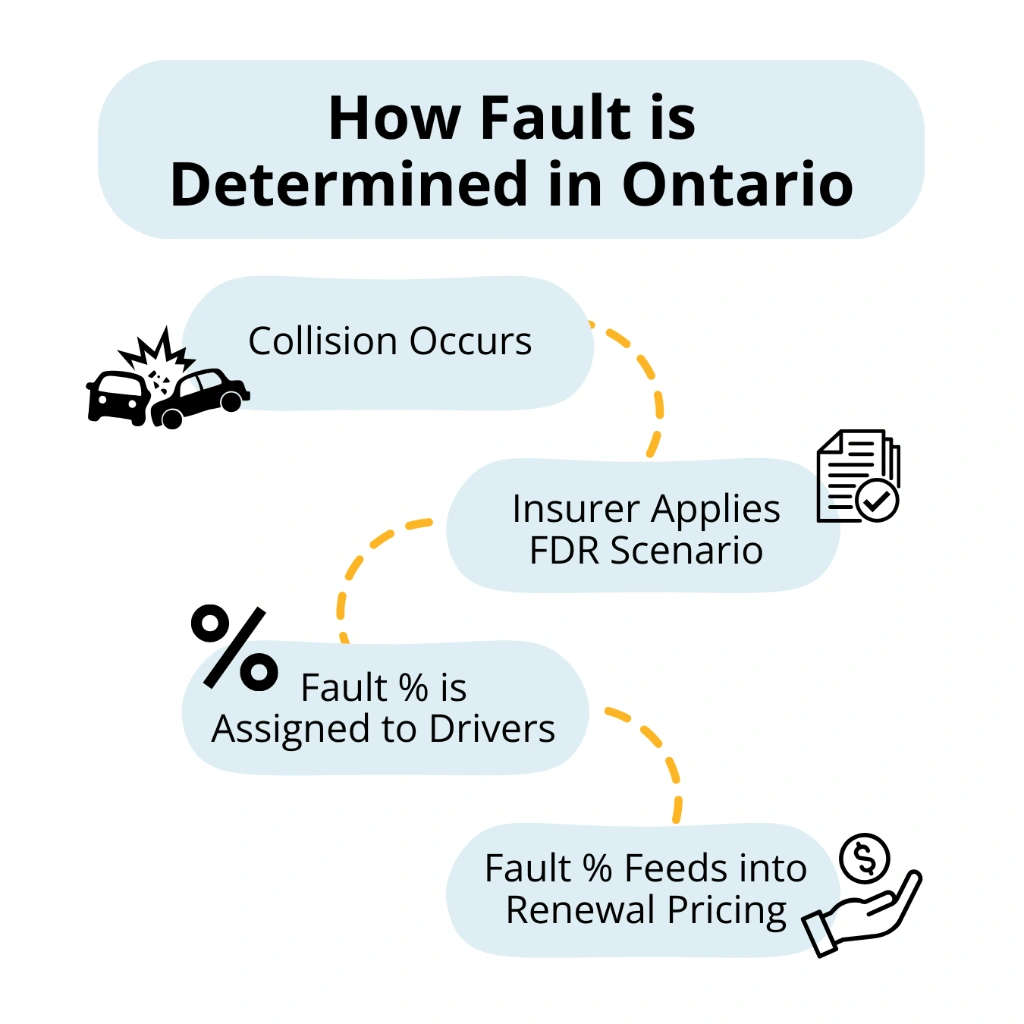

How is Fault Determined After Ontario Car Accidents?

After a car crash, Ontario insurers determine fault by using the official Fault Determination Rules (FDR) under the Insurance Act. Through this method, each driver involved in a collision is assigned a fault percentage between 0% and 100% based on the scenario. FDR outcomes commonly include 0%, 25%, 50%, 75%, or 100%.

When you’re involved in an accident, determining fault is extremely important so that insurers can assess whether a surcharge will apply to your premium and, in shared-fault situations, to what extent. The FDR includes over 40 illustrated scenarios which stipulate consistent outcomes for common types of collisions. For example:

- Rear-end collisions

- Left-turn impacts

- Intersection “T-bone” crashes

- Lane changes

- Parking lot incidents

- Multi-vehicle chain reactions

- And more

These rules apply to such scenarios regardless of weather, visibility, road conditions, or point of impact. In other words, citing “bad weather” or “surprise ice” is generally not a valid defence for fault under Ontario’s legal framework.

When determining fault in an accident, insurers will review driver statements, photographs and videos from the scene, police reports (if they exist), witness statements, and dashcam footage. They are detailed in their assessment because it is possible for fault to be split between drivers. For example:

- A lane-change collision on a busy highway may result in each driver being assigned 50% fault if both tried to merge unsafely.

- A multi-car chain reaction can lead to different percentages for different drivers, depending on the following distance prior to the crash and reaction time.

It is important to note that whether police charge (or do not charge) a driver under the Highway Traffic Act does not necessarily determine insurance fault. Insurance fault is based on how the accident matches the scenarios outlined in the FDR, not just on whether a ticket was issued.

How Does Fault Affect Car Insurance Premiums in Ontario?

Once fault is established after an accident, it can affect what happens to your insurance premiums upon the renewal of your policy:

- At-Fault: If you are found to be 50% or more at-fault for your accident, it is likely that you will see a surcharge added to your insurance premium at renewal. The average increase in premiums for at-fault drivers in Ontario is between 20% and 50%, although a 100% surcharge is possible for high-risk drivers or for drivers who have claimed multiple prior at-fault losses.

- Shared Fault: In some cases, each driver may be assigned partial fault for an accident (e.g., 25% or 50%). Partial fault can still influence your premium at renewal, depending on your insurer’s specific rating system and overall driver history.

- Not at Fault: If you are found to be 0% at-fault for the accident, your premium should not rise at all at renewal due to the collision. However, it is important to remember that unrelated factors (such as territory, vehicle changes, or broad market shifts) can still affect insurance rates upon renewal.

How Long Does an Accident Stay on Your Record?

When you are found to be at fault for an accident after making a claim, the entry can affect your premiums for several years after the collision. Claimants may see the heaviest impact in the first 24-36 months after their policy is renewed, with surcharges potentially tapering if the driver remains claim and conviction-free.

Can You Challenge Fault After an Accident?

If an insurer finds you to be at a level of fault that you don’t believe is fair, there are several steps you can take to challenge their decision.

You may ask the insurer to explain which specific FDR scenario was applied and dispute its suitability. You may also submit additional evidence, such as dashcam videos, independent witness statements, or clearer photographs of the accident, to contradict their findings.

In Ontario, official dispute resolution processes (including formal escalation) exist for drivers who disagree with insurer fault determinations. When undertaking these processes, working with a professional can be helpful.

What is Minor At-Fault Protection in Ontario?

If you are involved in one minor at-fault collision within three years, it is possible that your premium will not rise under certain conditions. To qualify as a minor at-fault crash, there must be:

- No injuries,

- No insurer payouts to either party, and

- Property/vehicle damage must be under $5,000 per vehicle or property.

This is referred to as minor at-fault protection in Ontario. As of July 1st, 2025, the $5,000 threshold aligns with the updated mandatory police reporting limit. It is important to note that minor at-fault protection differs from optional “accident forgiveness” endorsements that certain insurers offer to customers.

Estimated Premium Increase for At-Fault Drivers by Accident Severity (Ontario)

Ranges vary by insurer, claim history, and rating class. Consult with your insurer to determine your exact premium increase after a collision

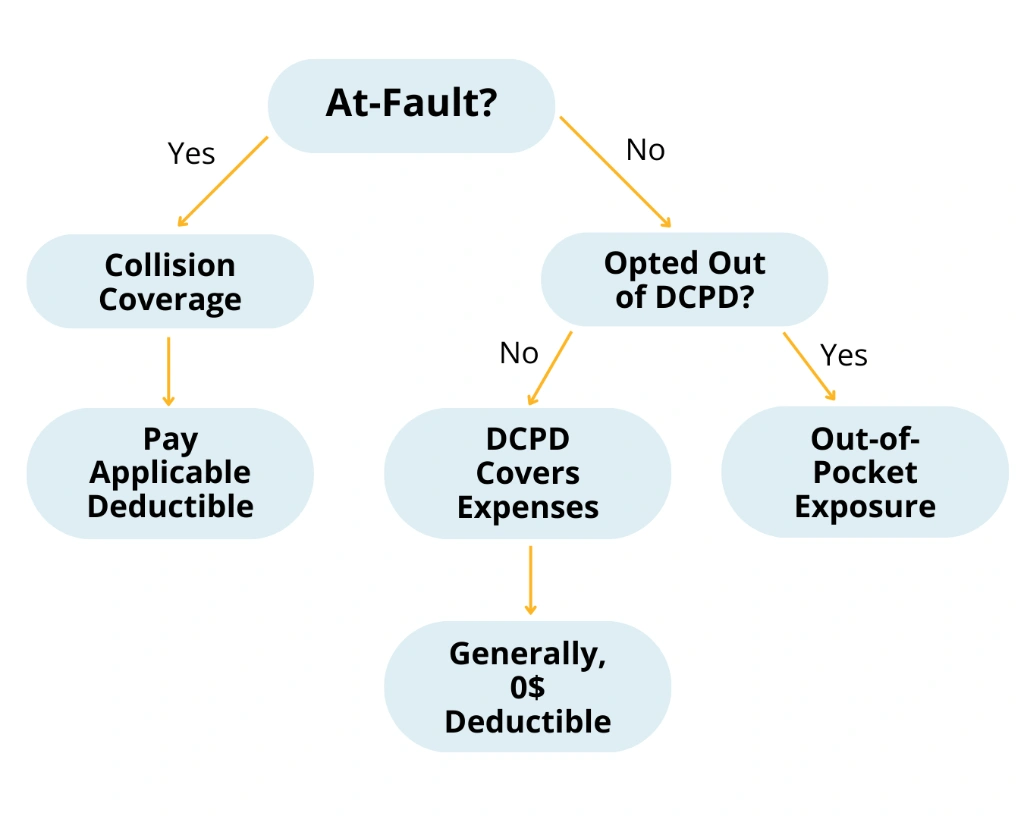

Coverage Interaction: DCPD, Collision Coverage, and Deductibles

Understanding how coverages apply after your car crash will help explain why some claims change your premium and others do not. In Ontario, some central property-damage coverages include:

Direct Compensation-Property Damage (DCPD)

DCPD generally applies when you are not at fault (0%) for an accident. It covers damage to your vehicle, certain contents, and loss of use. Since January 2024, Ontario drivers may opt out of DCPD coverage in their policy to reduce their premiums. Although doing so may lower the price of your insurance, it could increase the amount of out-of-pocket expenses you owe after an accident, even if you’re not at fault.

To be eligible for DCPD in Ontario, the at-fault vehicle must generally be identified and insured. If the other vehicle is unidentified (such as in a hit-and-run accident), DCPD may not apply.

Collision Coverage

Collision coverage is also sometimes called “upset” coverage. It is an optional form of coverage and typically applies when you are at fault for an accident or when no other applicable property-damage coverage applies (for example, in single-vehicle accidents, striking a fixed object, or hit-and-run scenarios).

A deductible almost always applies to collision coverage. This means you must pay a certain amount yourself before insurance begins to cover your expenses. If you do not have collision coverage and you are at fault for your accident, you generally must pay for repairs to your own vehicle out of pocket.

Shared Fault and Deductibles

Ontario uses percentage-based fault. When fault is shared between drivers (e.g., 50%/50%), the deductible they pay may scale according to fault. For example, if you are found to be 50% at fault and you have a $500 collision deductible, you may only pay $250. Deductible terms vary by policy, so it’s important you review the exact language in your contract when you make a claim.

Rules for Vehicle Lending

When driving in Ontario, auto insurance policies generally follow the vehicle, not the policyholder. If someone else is driving your car when a collision occurs, the claim will usually be recorded on your policy history and may affect your premium at renewal. This is true even if the driver is not a named insured on your policy.

Real-Life Scenarios & Coverage Interactions

Your fault assessment (made in accordance with the FDR) may determine the type of coverage you are eligible for after an accident. For example:

- Rear-Ended at a Stop: When you’re rear-ended while stopped, your fault is generally 0%. In this case, DCPD will typically address your vehicle damage and loss of use (assuming you did not opt out of DCPD coverage and you have identified the at-fault driver). You generally will not see any increases in your insurance premiums after claiming DCPD.

- Backing into a Pole: When you back into a pole, you may be found to be 100% at fault for the collision. In such a case, collision coverage (if you carry it) will often apply, with a deductible.

- Lane Change Contact: When drivers collide while changing lanes, fault may be divided evenly at 50% (depending on the circumstances). In these cases, DCPD may apply to the not-at-fault portion and collision coverage to the at-fault portion. The deductible you pay may also be proportional to your share of fault.

Which Coverage Applies After a Crash in Ontario?

Frequently Asked Questions: Ontario Car Insurance After an Accident

Below are some of the most frequently asked questions we get about car insurance rates in Ontario after an accident.

Will my premiums rise if my fault is only 25%?

Although it is not as likely, they can. Some insurers apply surcharges for any share of fault above 0%, not only 50% or more. Whether your premium increases will depend on the unique rating rules of your insurer and the terms of your policy.

How long does an at-fault accident affect insurance prices for?

In many cases, at-fault accident claims can affect the price of your insurance for several years following the incident. The most significant impact on rates is typically seen in the first two to three years, then it can begin to taper if you do not accumulate any further claims or convictions.

Does a not-at-fault claim change my premium?

If you are found 0% at fault under the FDR, the collision generally should not trigger a premium increase. However, your premium rates can still change upon renewal for other reasons unrelated to the accident.

What is Accident Forgiveness (OPCF 39)?

OPCF 39 is an accident forgiveness endorsement that stops your insurance premium from increasing after your first at-fault accident (so long as you meet the eligibility criteria). This is an optional form of coverage that you must purchase from your insurer. It is one-time, does not erase the accident from your record, and will not automatically transfer to a new insurer should you change your policy.

What happens after a hit-and-run accident?

You should report the incident as soon as possible. Depending on the type of coverage you have purchased and the facts of your case, your policy may still cover your damages. Although a hit-and-run claim does not automatically mean you will see a surcharge in your premium, insurers will still assess the circumstances of the accident to determine fault.

What if I’m involved in two at-fault collisions within three years?

If you are responsible for multiple at-fault collisions over a relatively short period of time, you may experience substantial surcharges. In many cases, you will also be treated as high-risk upon renewal. Premiums offered to ‘high-risk’ drivers are often significantly higher (sometimes double or more) compared to their pre-accident rate options.

More Frequently Asked Questions

Book a FREE Consultation

Tell us what happened

We’re here to help.

Speak With Our

Legal Team for FREE

Find Out if You Have a Case in Under 5 Minutes

Speak to a Lawyer Now!

We’re here to help.